- Jun 6, 2016

Why Student Loans are a Bad Idea, Especially for Music Majors

- Joseph @ Flex Lessons

After college, I learned quickly that the fun was over as I watched each student loan come out of deferment. Each new monthly payment meant less money at the end of the month, which brought about some anxiety. Are you considering student loans for college or know someone who is? Do you already have a few hanging around? If so, you might find my perspective helpful.

First, consider this Ted talk: How college loans exploit students for profit.

Although I don’t necessarily draw the same conclusions as the speaker, I find his points very insightful. He describes some of the less obvious problems with using student loans for college. Lack of planning can result in serious economic disadvantage, even after the degree is obtained. This is because you are encouraged to borrow amounts far greater than your ability to pay back. For this reason among many others, caution should be exercised when choosing your degree and dealing with student loans.

Student Loan Interest

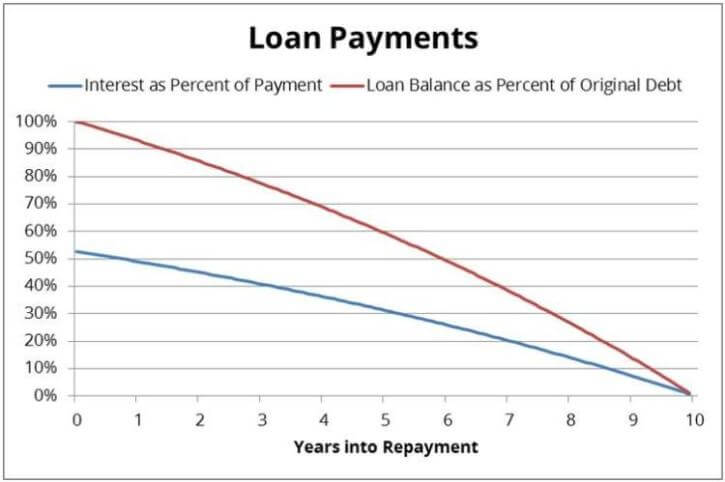

Many people don’t realize how much they pay in student loan interest. If you look at an amortization schedule for any loan, you will notice that much of the interest gets paid right in the beginning of the loan. This is because interest is calculated on the current borrowed amount. Until you pay your balance down, your payment will pay more interest than principle. Loans with 10 year terms and 6-7% interest rates end up costing quite a bit more than the amount originally borrowed. The chart below shows a typical 10 year loan and the percentage of yearly payments that are dedicated to interest.

10 Year Loan with 7.5% Interest Rate | www.edvisors.com

If your loans are unsubsidized and you choose not to make payments during your schooling, your loan balance will actually increase because interest will be capitalized (added to the balance of the loan). This results in you paying significantly more for your degree over time. Most of my loans were around 6.8%, and they grew by that percentage every year that they were in deferment (while I was in school and choosing not to pay them).

It is difficult to quantify the financial damage caused by student loan interest. You probably won’t notice the absence of the money, similar to how you might not pay attention to how much tax is withheld automatically from your paycheck. It adds up over time. However, you have a choice when it comes to using student loans for college. There are many ways to minimize your risk when considering loans.

How to Handle Student Loans for College

Here’s some tips based on what I have learned from my student loan experience:

Don’t use student loans for college. You can save up a few semesters worth of tuition and then pay the rest as you go.

Attend a public university. You shouldn’t pay for a private education without significant assistance from scholarships. The difference in quality of education is usually not large enough to justify the huge increase in cost.

If you have to borrow, limit how much you borrow. Borrow just what you need to cover your tuition and cash flow your other expenses such as fees and books. You should never borrow a total amount greater than your expected annual income after you leave school.

Work while you are in school. This allows you to avoid borrowing excess amounts to cover the cost of living. I highly recommend serving jobs while you are in school since serving jobs often have flexible hours and higher wages (including tips).

Pay the loan balances down while you are in school. Don’t let the interest become capitalized. Remember that you only pay interest on what is currently owed. If you pay down your balance, you owe less interest.

Once out of school, pay down the balances aggressively. Paying off loans early saves money on interest, unlocks the power of your income, and reduces your debt to income ratio which will allow you an easier path to financial prosperity.

Don’t default on a student loan. There is no reliable way out of a student loan other than dying (which we don’t want) because student loans are secured on your person. Student loans are protected from being discharged in a bankruptcy in most cases. One way or another, the banks will get their money, and the government will help them do it.

It is important to realize that student loans are not free money. Delaying your schooling by a semester or two and cash flowing your way through college would result in financial strength much earlier in life.

A Musician’s Experience

For those of you who are thinking about going to school soon, I hope you find my perspective helpful. Although I am happy with how my life ended up, I don’t recommend anyone take the same path (borrowing money for a music degree). I found it far too easy to borrow more than I needed. This article is written as if I had to do it all again.

If you have piled up a few loans already, I would recommend paying them off early and clearing your budget. By doing this, you can save quite a bit of money in interest and reduce your overall financial risk. As your income increases, resist the urge to raise your standard of living until you are debt free. Use any extra money to clear the debt. Whether you are a musician or not, you will benefit greatly by becoming debt free.

My preferred method of getting rid of student loans is to list the individual loans out and pay them off smallest to largest – Dave Ramsey’s snowball style. Did you know that you can pay extra on individual loans even if they are part of larger loans? Your monthly payments will decrease little by little until they are gone…no need for any consolidation.

I hope someone out there finds this perspective helpful. If you or someone you know would benefit from this post, please share.